Commercial Property Value Calculator

Calculation Results

When you're looking at a commercial property, the price isn't just about square footage or how nice the lobby looks. The real number comes down to one thing: rental income. That’s what drives value in office buildings, retail centers, warehouses, and medical offices. If you understand how to turn rent payments into a dollar value, you’re not just guessing-you’re investing with confidence.

What drives commercial property value?

Unlike homes, where buyers often compare similar houses in the neighborhood, commercial properties are valued based on cash flow. A 10,000-square-foot office building isn’t worth more just because it has marble floors. It’s worth what it earns. If it brings in $200,000 a year in rent and has low vacancies, it’s far more valuable than a similar building that’s half empty. Investors buy commercial properties to generate income, not just to own space.

The key metric here is Net Operating Income (NOI). This isn’t your profit after taxes or mortgage payments. It’s the money left over after you pay for the building’s day-to-day expenses-property taxes, insurance, maintenance, management fees, utilities, and repairs. You don’t subtract the mortgage. That’s because financing varies from buyer to buyer. NOI shows what the property itself earns, regardless of who owns it.

Let’s say a retail center collects $360,000 in annual rent. But it costs $90,000 to keep it running: $40,000 in taxes, $15,000 in insurance, $20,000 in repairs, and $15,000 in management. That leaves you with $270,000 in NOI. That’s the number that matters.

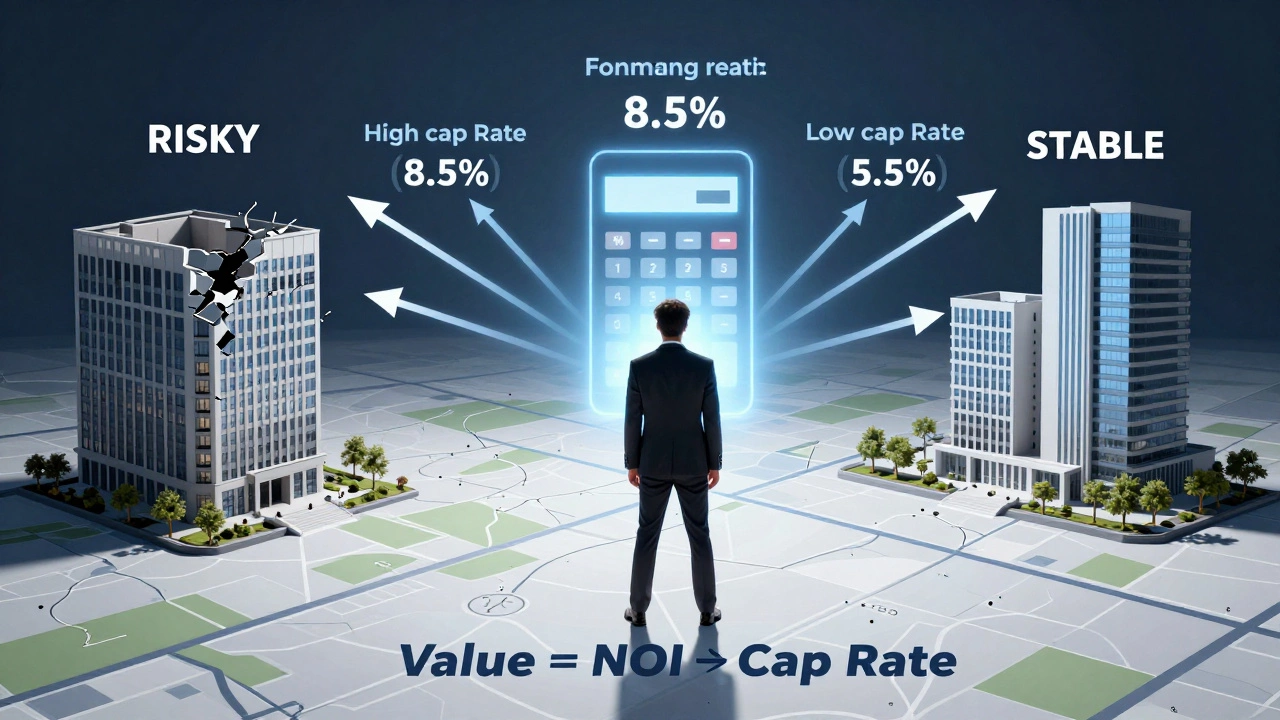

The cap rate: the simplest way to value a property

Once you have NOI, you use the capitalization rate-called the cap rate-to estimate value. This is a percentage that tells you how much return an investor expects to get from the property each year. It’s not a fixed number. It changes based on location, property type, and market conditions.

Cap rates for office buildings in downtown Chicago might be 5.5%. In a smaller city, they could be 7%. A newer warehouse in a logistics hub might trade at 5%, while an older strip mall in a declining area could be 8% or higher. The higher the cap rate, the riskier the investment-and the lower the price.

To find value, you divide NOI by the cap rate:

Property Value = NOI ÷ Cap Rate

Using the retail center example: $270,000 NOI ÷ 6% cap rate = $4,500,000 value.

If the cap rate jumps to 7%, the value drops to $3,857,000. That’s a $643,000 swing just from a 1% change. That’s why knowing the right cap rate matters more than almost anything else.

How to find the right cap rate for your property

You can’t just guess a cap rate. You need to look at what similar properties have actually sold for. Real estate data platforms like CoStar, Reonomy, or local broker reports show recent sales. Look for properties that are:

- The same type (e.g., single-tenant retail vs. multi-tenant strip center)

- In the same market or neighborhood

- Similar age and condition

- With comparable lease terms

For example, if three similar retail centers in your city sold last year with NOI of $250,000-$290,000 and sold for $3.8M-$4.2M, that gives you a cap rate range of 6.2% to 6.8%. You can then use the midpoint-say, 6.5%-as your benchmark.

Don’t rely on online calculators that use national averages. A cap rate of 5.8% might work for a Class A office tower in San Francisco, but it’s wildly off for a warehouse in Ohio. Local data is everything.

What if the property has vacancies?

Many commercial properties aren’t 100% occupied. That’s normal. But you can’t use the full rent amount in your NOI calculation. You need to account for vacancy loss.

Let’s say a building has 20,000 sq ft and leases for $20/sq ft annually. That’s $400,000 in potential rent. But 10% of the space is empty. That means you lose $40,000 in rent. Your effective gross income is $360,000. Then subtract operating expenses-say $95,000-and your NOI is $265,000.

Most investors use a 5%-10% vacancy allowance for stabilized properties. If a building has been empty for over a year, you’ll need to adjust your expectations. A property with long-term vacancies might need a higher cap rate to reflect the risk of finding new tenants.

Lease terms matter more than you think

A property with a 10-year lease from a national chain like CVS or Walgreens is worth more than one with month-to-month tenants. Why? Because long-term leases mean predictable income. Investors pay a premium for stability.

Look at lease expiration dates. If 80% of the rent comes from leases expiring in the next 12 months, you’re taking a big risk. You might have to lower rents to fill space, or pay for tenant improvements. That uncertainty lowers value.

On the flip side, if leases are locked in for 5+ years with annual rent increases (called escalations), the property’s value increases. Those escalations mean NOI will grow over time, making the asset more valuable.

Other factors that change value

Cap rate and NOI are the foundation-but other things shift the needle:

- Location: A medical office in a growing suburb beats one in a fading downtown.

- Building condition: A roof that needs replacing in two years? That’s a $150,000 hit to value.

- Tenant quality: A tenant with a strong credit rating (like Amazon or Kaiser Permanente) adds value. A tenant with a history of late payments? It’s a red flag.

- Zoning: Can you expand? Add more floors? Change use? Zoning flexibility can double value.

- Market trends: If e-commerce is killing retail, a standalone shopping center might drop 30% in value over three years.

These don’t change the cap rate formula-but they affect what cap rate you should use. A property with great tenants and long leases in a growing area might deserve a 5.5% cap rate. One with shaky tenants and a crumbling facade? Maybe 8.5%.

What to do if you’re unsure

If you’re not a professional investor, don’t try to guess cap rates or calculate NOI on your own. Hire a commercial appraiser. They’ll look at recent sales, analyze leases, assess condition, and give you a written report. It costs $1,500-$5,000, but it’s cheaper than overpaying by $500,000.

Or work with a commercial broker who specializes in your property type. They know the local market and can tell you what similar buildings are trading for right now. Don’t rely on Zillow or Redfin-they don’t track commercial deals accurately.

Real example: A small retail center in Austin, 2025

A 12-unit strip center in Austin, Texas, has 35,000 sq ft. It rents for $22/sq ft, totaling $770,000 in gross rent. Vacancy is 6%, so $46,200 is lost. Effective gross income: $723,800.

Operating expenses:

- Property taxes: $180,000

- Insurance: $35,000

- Maintenance: $48,000

- Management: $55,000

- Utilities: $22,000

Total expenses: $340,000

NOI: $723,800 - $340,000 = $383,800

Recent sales of similar centers in Austin show cap rates between 5.8% and 6.4%. The average is 6.1%.

Value: $383,800 ÷ 0.061 = $6,291,803

That’s the price range a buyer should consider. If the seller wants $7 million, they’re asking for a premium. If they’re asking for $5.5 million, it’s a bargain.

Final rule: Always check the data

There’s no magic formula. No shortcut. The only way to know a commercial property’s true value is to look at real numbers-actual rent, real expenses, real sales. Don’t trust online tools that ask for zip codes and spit out a number. Commercial real estate doesn’t work like that.

Use NOI. Use cap rates from local comps. Understand lease terms. Watch for hidden costs. And always, always ask: What’s the income doing, not what the building looks like?

Can I use the same method to value a residential property?

No. Residential properties are usually valued based on comparable sales-what similar homes sold for nearby. While rental income can be a factor for multi-family buildings (like duplexes or small apartment complexes), single-family homes rarely use NOI or cap rates. Commercial properties rely on income because they’re bought as investments, not as places to live.

What’s a good cap rate for commercial property?

There’s no universal number. In 2026, cap rates range from 4.5% for Class A office towers in major cities to 8% or higher for older retail or industrial buildings in secondary markets. A cap rate between 5.5% and 7% is common for stable, well-located properties. Higher cap rates mean higher risk or lower prices. Lower cap rates mean more competition and higher prices.

Does the mortgage affect the property’s value?

No. When calculating value from rental income, you ignore the mortgage entirely. That’s because the property’s value should be the same whether you pay cash or take out a loan. The mortgage affects your cash flow and return on investment-but not the underlying value of the asset. That’s why NOI excludes debt service.

How often should I recalculate the value?

Update your estimate every 6 to 12 months. Rental rates, operating costs, and cap rates change. If a new competitor opens nearby, or if your main tenant renews at a lower rate, your property’s value shifts. Regular updates help you make better decisions-whether you’re selling, refinancing, or just tracking performance.

Can I value a property with only one tenant?

Yes. Single-tenant properties (like a standalone Starbucks or Dollar General) are common. Their value depends heavily on the tenant’s creditworthiness and lease length. A 15-year lease with a national chain and annual rent increases can command a lower cap rate (maybe 5%) because it’s low-risk. A single tenant with a weak credit rating and a 2-year lease might need a cap rate of 7.5% or higher.