Self-Rent Amount Calculator

Why This Matters

Using a realistic market rent is crucial for ATO compliance when claiming home office deductions. The ATO compares your rent amount against market rates, and inconsistent or artificially low amounts can trigger audits.

Input Your Property Details

Results & Recommendations

Why This Amount?

The ATO compares your claimed rent against market rates. This calculation is based on average rental prices for similar properties in your area, adjusted for condition.

How to Use This Result

1. Use this rent amount consistently in your self-rent agreement

2. Transfer this amount monthly from your personal account to a separate business account

3. Label your transfers with "Monthly rent payment for [address]"

4. Keep bank statements for at least 5 years

Most people think a rent agreement is something you sign with a landlord. But what if you’re the landlord? What if you’re the tenant? And what if you’re both - at the same time?

This isn’t a trick. It’s called a self-agreement - a written contract between yourself as landlord and yourself as tenant. It sounds strange, but it’s not uncommon in Australia, especially for people who own property but live in it under a formal rental structure. Whether you’re trying to claim tax deductions, protect your assets, or simply bring clarity to your living situation, making a rent agreement with yourself can be smart. And yes, it’s legal.

Why Would You Rent to Yourself?

Let’s say you own a property in Melbourne. You live in it. But you also run a small business from home - maybe you’re a freelance designer, a coach, or a consultant. The ATO allows you to claim a portion of your home expenses as business deductions: electricity, internet, rates, even depreciation on furniture. But to do that properly, you need to show a clear separation between personal and business use.

That’s where the self-agreement comes in. By treating your home as if you’re renting part of it to your own business, you create a paper trail that the tax office accepts. It’s not about cheating the system. It’s about following the rules cleanly.

Another reason? Asset protection. If you own your home in a trust or company, and you’re living in it, the ATO might question whether you’re truly paying market rent. A signed agreement shows you’re treating it like a legitimate business arrangement - not just a personal perk.

And if you’re planning to sell later? Having a documented rental history can help prove you weren’t just living there rent-free. It adds legitimacy to your claims.

What Goes Into a Self-Agreement?

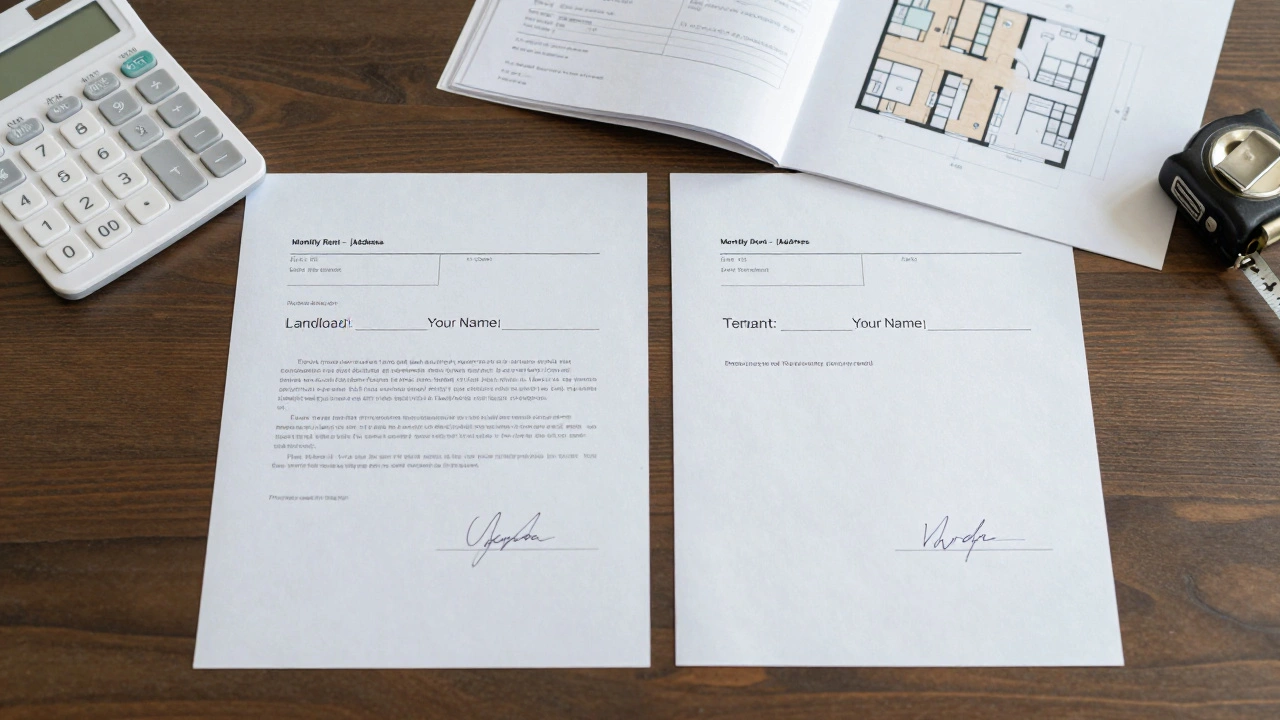

A rent agreement with yourself doesn’t need to be fancy. But it does need to be real. Here’s what you must include:

- Parties involved: Clearly state “Landlord: [Your Full Name]” and “Tenant: [Your Full Name]”. Use the same name both times - no aliases.

- Property address: The full legal address of the property. Include the lot and plan number if you have it.

- Rent amount: This must be a realistic market rate. Don’t pick $1 a month. Check Rent.com.au or Domain for similar properties in your suburb. For example, if a 3-bedroom house in Brunswick rents for $2,800/month, that’s your number. Use that figure consistently across all documents.

- Payment method: Even though it’s you paying yourself, you need to record it. Set up a bank transfer from your personal account to a separate business account. Keep the receipts. No cash. No “I’ll just write it down.”

- Lease term: One year is standard. You can renew it annually. This shows you’re treating it as a real, ongoing arrangement.

- Responsibilities: Who pays for repairs? Who handles gardening? Who pays water rates? Be specific. If you’re the landlord, you’re responsible for structural repairs. If you’re the tenant, you’re responsible for minor maintenance.

- Business use clause: If you’re claiming home office deductions, list the exact square metres used for business. Include a simple floor plan if possible. The ATO accepts this if it’s reasonable - say, 10% of a 200m² house = 20m².

Don’t forget to date it. Sign it. Print two copies. Keep one in your personal file. Keep one in your business file. Treat it like any other legal document.

How to Set the Right Rent Amount

This is the most common mistake. People pick a number that feels “fair” - like $500 a month - because they’re “just helping themselves.” That won’t fly with the ATO.

Here’s how to get it right:

- Search for similar properties on Domain or Rent.com.au. Filter by bedrooms, location, and property type.

- Look at the median rent for the last 6 months. Don’t use the highest or lowest.

- Adjust for condition. Is your place newer? Better furnished? Add 5-10%. Older or needing work? Subtract 5%.

- Write down the number. Stick to it. Don’t change it every year unless market conditions shift significantly.

For example, in Footscray in 2025, a 2-bedroom unit with a small backyard rents for around $2,400/month. If you live there, that’s your number. Even if you’re the owner.

Why does this matter? Because the ATO cross-checks. If you claim $1,800 in home office deductions but your rent is only $600/month, they’ll question it. If your rent is $2,400/month and you’re claiming 15% ($360/month), it looks logical. Consistency is everything.

How to Record Payments

You’re paying yourself. So how do you prove it?

Open a separate bank account for your business - even if you’re a sole trader. Name it something like “[Your Name] Business Operations.”

Every month, transfer the rent amount from your personal account to your business account. Add a note: “Monthly rent payment for [address].”

Keep the bank statement. Print it. File it. Don’t rely on digital records alone. The ATO asks for paper trails.

And yes - your business account will now have income. That means you need to declare it as income on your tax return. But here’s the balance: you can then claim all the expenses tied to that rental income - mortgage interest, insurance, council rates, repairs, cleaning, even the cost of the agreement itself.

It’s not about making money. It’s about balancing the books properly.

What Happens If You Don’t Do This?

Many people skip this step. They claim home office deductions without a formal agreement. They get away with it - for a while.

But if you’re ever audited - and the ATO audits about 1 in 20 small business owners - you’ll need to prove your claims. Without a signed agreement, you’re relying on memory. Or worse, a spreadsheet you made in 2023.

One client in Richmond lost $8,000 in claimed deductions because they couldn’t prove they were paying rent to themselves. The ATO said: “If you didn’t pay yourself rent, you didn’t have a rental arrangement. Therefore, no deductions.”

It’s not about being paranoid. It’s about being prepared.

Common Mistakes to Avoid

- Using a handwritten note: A typed, signed document looks professional. Handwritten = informal. The ATO notices.

- Changing rent every year: Unless market rates shift, keep it stable. Frequent changes look artificial.

- Not using a separate bank account: Mixing personal and business money is a red flag.

- Claiming 100% of expenses: You can’t claim your entire mortgage if you’re living there. Only the portion used for business.

- Forgetting to renew: If your agreement expires and you don’t sign a new one, the ATO may say the arrangement ended.

When This Doesn’t Make Sense

This isn’t for everyone. If you’re a regular employee who works from home 2 days a week, you don’t need a formal rent agreement. You can use the simplified method: 67 cents per hour for home office costs. It’s easier and just as valid.

Self-agreements are for:

- Business owners operating from home full-time

- People who own property through a trust or company

- Those claiming significant deductions (over $2,000/year)

- People planning to sell soon and want clean records

If you’re just working from your kitchen table, stick with the 67-cent rule. No need to overcomplicate it.

Final Checklist

Before you sign your self-agreement, run through this:

- ✅ Rent amount matches market value (verified with Domain/Rent.com.au)

- ✅ Agreement is typed, signed, dated, and printed in two copies

- ✅ Bank transfers are made monthly and labeled clearly

- ✅ Business use area is measured and documented (with photo or sketch)

- ✅ You’re claiming only the percentage tied to business use

- ✅ You’ve told your accountant about it

That’s it. No magic. No loopholes. Just clear, simple, legal steps.

Making a rent agreement with yourself isn’t about tricking the system. It’s about being honest with it. You own the property. You live in it. You use part of it for work. You pay rent. You claim deductions. Everything lines up. That’s not clever. That’s responsible.

And in a system that rewards clarity over confusion, that’s the smartest move you can make.

Can I really make a rent agreement with myself?

Yes. The Australian Taxation Office (ATO) accepts a written rental agreement between yourself as landlord and yourself as tenant, as long as it’s realistic, documented, and followed consistently. This is commonly used by business owners who work from home and want to claim legitimate tax deductions.

Do I need to pay myself rent every month?

Yes. To prove the arrangement is real, you must transfer rent money from your personal account to a separate business account each month. Even though it’s your own money, the transaction creates a paper trail the ATO requires. No cash. No notes. Real bank transfers.

What rent amount should I use?

Use the current market rent for a similar property in your area. Check Domain or Rent.com.au for median rents of homes with the same number of bedrooms, location, and condition. Don’t pick a low number to save tax - the ATO compares your claim to market data.

Can I claim 100% of my rent as a business expense?

No. You can only claim the portion of your home used for business. If you use one room out of five for work, that’s 20%. Use floor plans or measurements to support your claim. Claiming more than your actual business use risks an audit.

Do I need a lawyer to draft this agreement?

No. A simple, typed document with all key details - parties, address, rent, term, responsibilities - is enough. Many templates are available online for free. Just make sure it’s signed, dated, and you keep two copies. A lawyer isn’t required unless your situation is complex (e.g., trust ownership).

What if I sell my home later?

Having a documented rental agreement helps prove you weren’t living in the property rent-free. This can support your claim for the main residence exemption from capital gains tax, especially if you used part of the home for business. Keep all records for at least five years after selling.